All Categories

Featured

Table of Contents

Variable annuities have the capacity for higher earnings, yet there's even more danger that you'll lose cash. Be careful concerning putting all your assets right into an annuity. Representatives and companies have to have a Texas insurance policy certificate to legally market annuities in the state. The problem index is an indicator of a company's client solution record.

Annuities sold in Texas needs to have a 20-day free-look period. Replacement annuities have a 30-day free-look duration.

The amount of any kind of abandonment charges. Whether you'll lose any type of bonus offer rate of interest or features if you surrender your annuity. The guaranteed rate of interest of both your annuity and the one you're taking into consideration changing it with. Just how much cash you'll require to begin the new annuity. The lots or payments for the brand-new annuity.

Ensure any kind of agent or firm you're thinking about purchasing from is accredited and monetarily secure. annuity type. To verify the Texas license standing of an agent or business, call our Aid Line at 800-252-3439. You can also utilize the Firm Lookup attribute to find out a business's financial score from an independent score organization

There are 3 kinds of annuities: taken care of, variable and indexed. With a fixed annuity, the insurance provider assures both the price of return (the rate of interest) and the payment to the investor. The rates of interest on a dealt with annuity can transform gradually. Commonly the rate of interest price is repaired for a number of years and afterwards adjustments periodically based on current rates.

Insurance Annuity Rates

With a deferred fixed annuity, the insurance provider accepts pay you no less than a defined interest rate throughout the time that your account is growing (annuity risks). With an instant fixed annuityor when you "annuitize" your postponed annuityyou receive a predetermined fixed quantity of money, typically on a month-to-month basis (similar to a pension plan)

While a variable annuity has the benefit of tax-deferred development, its annual costs are most likely to be much greater than the expenses of a typical common fund. And, unlike a dealt with annuity, variable annuities don't supply any guarantee that you'll make a return on your financial investment. Instead, there's a danger that you could actually lose cash.

Due to the complexity of variable annuities, they're a leading source of capitalist issues to FINRA (buying annuity). Before acquiring a variable annuity, carefully read the annuity's syllabus, and ask the person marketing the annuity to describe all of the item's attributes, motorcyclists, costs and constraints. You need to also know exactly how your broker is being compensated, including whether they're obtaining a commission and, if so, just how much

Annuity Types Explained

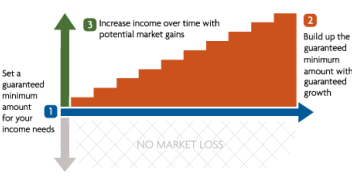

Indexed annuities are intricate economic tools that have features of both taken care of and variable annuities. Indexed annuities typically provide a minimum guaranteed rate of interest integrated with a passion rate linked to a market index. Several indexed annuities are connected to broad, widely known indexes like the S&P 500 Index. But some use various other indexes, including those that represent various other sections of the market.

Comprehending the functions of an indexed annuity can be confusing (lump sum annuities). There are several indexing approaches firms use to compute gains and, as a result of the range and intricacy of the methods used to credit report rate of interest, it's hard to contrast one indexed annuity to one more. Indexed annuities are generally categorized as one of the complying with two types: EIAs use an assured minimum rate of interest (generally at the very least 87.5 percent of the premium paid at 1 to 3 percent rate of interest), along with an extra rate of interest connected to the performance of several market index

Rates are since day and are subject to transform. 5. The S&P 500 Index consists of 500 big cap stocks from leading business in leading sectors of the U.S. economic climate, catching around 80% insurance coverage of U.S. equities. The S&P 500 Index does not consist of rewards stated by any one of the firms in this Index.

The LSE Group makes no claim, forecast, warranty or representation either regarding the outcomes to be gotten from IndexFlex or the viability of the Index for the purpose to which it is being placed by New York Life. Variable annuities are long-lasting economic items used for retirement savings. There are charges, expenses, limitations and dangers connected with this plan.

Withdrawals might be subject to normal income taxes and if made prior to age 59 might be subject to a 10% Internal revenue service penalty tax obligation. This material is basic in nature and is being provided for educational objectives just.

The syllabus have this and various other details regarding the product and underlying financial investment choices. In the majority of jurisdictions, the policy kind numbers are as adheres to (state variants may apply): New York Life IndexFlex Variable AnnuityFP Series (ICC20V-P02 or it may be NC20V-P02).

Variable Annuity Contract

A revenue annuity starts dispersing payments at a future day of your option. Usually, you make a single lump-sum settlement (or a collection of settlements) and wait till you're ready to begin obtaining earnings. The longer your cash has time to grow, the higher the earnings repayments will certainly be. Repaired deferred annuities, also referred to as repaired annuities, give steady, surefire growth.

The worth of a variable annuity is based upon the performance of a hidden portfolio of market investments. annuity rates comparison. Variable annuities have the advantage of supplying more selections in the method your cash is spent. This market direct exposure may be required if you're trying to find the possibility to expand your retired life nest egg

This material is for details use just. It must not be depended on as the basis to buy a variable, taken care of, or instant annuity or to apply a retirement approach. The info supplied here is not created or intended as investment, tax, or legal recommendations and might not be counted on for objectives of staying clear of any kind of federal tax obligation charges.

Tax results and the relevance of any kind of item for any kind of details taxpayer may differ, relying on the particular set of realities and situations. Entities or individuals dispersing this information are not licensed to give tax obligation or lawful suggestions. Individuals are encouraged to seek details advice from their individual tax obligation or lawful advice.

If withdrawals are taken before age 59, a 10% IRS charge might additionally use. Withdrawals may additionally go through a contingent deferred sales charge. Variable annuities and their underlying variable investment choices are marketed by prospectus only. Capitalists should take into consideration the investment objectives, risks, fees, and costs thoroughly prior to spending.

Are Annuities Good For Retirees

Please read it before you invest or send out cash. Taken care of and variable annuities are issued by The Guardian Insurance Policy & Annuity Firm, Inc. (GIAC). All guarantees are backed exclusively by the stamina and claims-paying ability of GIAC. Variable annuities are provided by GIAC, a Delaware company, and dispersed by Park Avenue Securities LLC ().

5 Watch out for dealt with annuities with a minimal surefire rate of interest of 0%. You will certainly not lose principal, but your cash will certainly not grow. You will not obtain all the added passion that the supply market could make. us life annuity. The insurer chooses just how much you obtain. Look out for advertisements that reveal high interest prices.

Some annuities use a higher guaranteed passion for the very first year just. This is called a teaser price. The interest decreases afterwards. Ensure to ask what the minimal price is and the length of time the high rate of interest lasts. There are various means to begin getting earnings payments.

What Percentage Do Annuities Pay

You generally can not take any type of added cash out. The primary factor to acquire a prompt annuity is to obtain a routine earnings right now in your retired life. Deferred Annuity: You begin getting revenue several years later on, when you retire. The primary reason to purchase a deferred annuity is to have your money grow tax-deferred for some time.

This material is for educational or instructional functions only and is not fiduciary financial investment advice, or a securities, investment method, or insurance item referral. This material does not think about an individual's very own goals or circumstances which must be the basis of any investment decision. Financial investment items might be subject to market and various other danger factors.

{kind=link}

Table of Contents

Latest Posts

Breaking Down Variable Annuity Vs Fixed Annuity Key Insights on Variable Vs Fixed Annuities Breaking Down the Basics of Investment Plans Advantages and Disadvantages of Different Retirement Plans Why

Understanding Financial Strategies A Closer Look at Choosing Between Fixed Annuity And Variable Annuity What Is the Best Retirement Option? Features of Fixed Vs Variable Annuities Why Choosing the Rig

Exploring the Basics of Retirement Options Key Insights on Your Financial Future Defining Pros And Cons Of Fixed Annuity And Variable Annuity Benefits of Choosing the Right Financial Plan Why Choosing

More

Latest Posts